Storm season has a way of exposing weaknesses. Not just in roofs, gutters, and siding, but also in insurance estimates. After a severe hailstorm, many homeowners assume the insurance company’s first estimate represents the full amount needed to restore their property. Unfortunately, that is often not the case. Hail Damage Claim Supplements: What Carriers Miss in Their Scope is a topic that deserves attention because overlooked damage and missing line items can leave property owners responsible for expenses they never expected.

I’ve reviewed countless hail claims over the years, and one pattern appears repeatedly. The initial insurance estimate frequently misses components, underestimates labor, overlooks code requirements, or fails to account for hidden damage. The result? A settlement that falls short of what is actually required to return the property to its pre-loss condition.

This is where claim supplements become incredibly important. When properly documented and supported through detailed Xactimate estimates, supplements can uncover legitimate costs that should have been included from the beginning. The process is not about inflating claims. It is about accuracy. Let’s examine what carriers commonly miss and how professional Xactimate expertise can help identify those gaps.

What Is a Hail Damage Claim Supplement?

A supplement is an additional request for payment submitted after an initial estimate has been issued.

Supplements typically arise when:

- Additional damage is discovered

- Repair requirements become clearer

- Code upgrades are identified

- Measurements are corrected

- Missing line items are documented

Think of the initial insurance estimate as the first draft. The supplement process refines that draft into a more complete and accurate scope of repairs.

Why Supplements Are So Common

Hailstorms often generate hundreds or even thousands of claims in a concentrated geographic area. Adjusters are under pressure. Inspection schedules become packed. Deadlines become tight. As a result, inspections sometimes focus on identifying obvious damage rather than documenting every repair component required for restoration. That is not necessarily negligence. It is simply a reality of catastrophe claim handling.

Why Initial Insurance Scopes Are Frequently Incomplete

Many homeowners are surprised when contractors identify thousands of dollars in additional repairs that were not included in the carrier’s estimate. The reasons are often straightforward.

Limited Inspection Time

An adjuster may only spend a short period evaluating an entire property.

During that inspection, they are expected to assess:

- Roofing

- Gutters

- Siding

- Windows

- Exterior accessories

- Ventilation systems

- Flashings

- Outbuildings

That is a substantial amount of information to capture in a limited timeframe.

Catastrophe Claim Volume

Following major storms, insurers frequently deploy catastrophe teams. These professionals may inspect dozens of properties each week. The goal is efficiency. The challenge is detail. Even highly experienced adjusters can miss components when handling large claim volumes.

Hidden Damage Cannot Always Be Seen

Some hail-related issues simply do not reveal themselves during an initial inspection.

Examples include:

- Underlayment damage

- Mat fractures

- Flashing deterioration

- Ventilation issues

- Decking concerns

These items often emerge later during repairs.

Understanding Xactimate and Why It Matters

Most major insurance carriers use Xactimate as their estimating platform. It is the industry standard. Every line item, measurement, labor category, and material cost is entered into the software to create a detailed repair estimate. However, software is only as accurate as the information entered into it. That distinction matters.

What Xactimate Actually Does

Xactimate helps estimate:

| Category | Examples |

| Roofing | Shingles, ridge caps, underlayment |

| Exterior | Gutters, siding, paint |

| Labor | Installation, tear-off, cleanup |

| Equipment | Lifts, dumpsters, safety equipment |

| Specialty Items | Flashing, vents, accessories |

The software itself does not determine what should be included. The estimator does.

Why Xactimate Expertise Matters

Two people can inspect the same roof. Both can use Xactimate. Both can generate estimates. Yet the estimates may differ by thousands of dollars.

Why? Because one estimator identifies every necessary component while the other overlooks certain requirements.

The software is a tool. Experience drives the outcome. Like many advanced estimating platforms, Xactimate relies on large datasets, pricing databases, and structured calculations. In some ways, this process resembles the use of a Bayesian network in decision-making systems, where multiple variables are analyzed to support more accurate outcomes.

Common Roofing Components Carriers Miss

One of the most frequent supplement categories involves roofing components that were simply omitted from the original scope. These omissions may seem small individually. Collectively, they add up quickly.

Starter Shingles

Starter shingles are installed along roof edges to improve wind resistance and create proper sealing. Many initial estimates fail to include them. Without starter materials, proper installation becomes difficult.

Ridge Cap Shingles

Ridge caps protect roof peaks and help maintain system integrity. Carriers sometimes underestimate quantities or omit them entirely. That creates an immediate shortfall.

Hip and Ridge Components

Modern roofing systems often require specific products for hips and ridges. These components carry separate costs that should be reflected in the estimate.

Underlayment

Underlayment serves as a secondary moisture barrier beneath the shingles. Depending on the roof system, replacement may be necessary after hail damage. Failure to include underlayment can significantly reduce the estimate’s accuracy.

Flashing Components Frequently Overlooked

Flashing protects vulnerable transition points throughout the roofing system. It is essential. Yet flashing-related omissions are among the most common supplement requests.

Commonly Missed Flashing Items

- Step flashing

- Headwall flashing

- Counter flashing

- Valley metal

- Pipe jack flashing

- Chimney flashing

These materials are critical for water management. Ignoring them can create long-term leak risks.

Why Flashing Gets Missed

Flashing is often partially concealed. Inspectors may not be able to evaluate every component without additional access or partial removal. As a result, flashing replacement frequently becomes a supplement issue.

Ventilation Components Often Missing From Estimates

Roof ventilation affects both performance and longevity. Unfortunately, ventilation systems are sometimes overlooked during hail inspections.

Common omissions include:

- Ridge vents

- Turtle vents

- Turbine vents

- Exhaust vents

- Powered attic ventilators

When damaged components remain in place, roof performance may suffer. Proper supplementation ensures these systems are addressed.

Soft Metal Damage: A Major Indicator

Soft metals often provide some of the strongest evidence supporting hail claims. Hail leaves visible marks. These impacts can help confirm storm-related damage.

Areas Frequently Impacted

| Soft Metal Component | Common Damage |

| Gutters | Dents |

| Downspouts | Impact marks |

| Vent covers | Surface deformation |

| Flashings | Dents and bends |

| Drip edge | Visible impact damage |

These indicators often support broader roofing damage findings. However, carriers sometimes exclude certain soft metal repairs from their scope. Supplements help address those omissions.

Hidden Hail Damage That May Not Appear Immediately

Not all hail damage is obvious. Some forms remain hidden beneath the surface.

Shingle Bruising

Bruising occurs when hail impacts weaken the underlying mat. The damage may not appear severe initially. Over time, however, deterioration can accelerate.

Granule Loss

Protective granules shield shingles from ultraviolet exposure. When hail removes those granules, shingles become more vulnerable to aging and weathering.

Mat Fractures

Mat fractures can compromise the structural integrity of roofing materials. These fractures are often difficult to identify without close inspection. Because they are less visible, they are frequently involved in supplement requests.

Building Code Requirements Commonly Missing

Modern building codes evolve constantly. What was acceptable twenty years ago may no longer meet current requirements. That matters during insurance restoration projects.

Examples of Code-Related Supplement Items

- Drip edge installation

- Enhanced underlayment requirements

- Ventilation upgrades

- Flashing improvements

- Fastener requirements

When local codes require these upgrades, additional costs may become part of the claim.

Why Carriers Miss Code Items

Code requirements vary by jurisdiction. An estimate prepared quickly may not fully account for local enforcement standards. This becomes particularly important in storm-prone areas such as League City, where roofing systems must withstand challenging weather conditions.

Measurement Errors That Can Reduce Settlements

One of the simplest ways a claim becomes undervalued is through inaccurate measurements. Even small errors can create significant differences.

Common Measurement Problems

- Missing roof facets

- Incorrect pitch calculations

- Inaccurate waste factors

- Omitted dormers

- Overlooked valleys

A few squares of roofing material may not sound significant.

Yet those differences affect:

- Labor

- Materials

- Disposal costs

- Delivery fees

- Accessory items

Every measurement matters.

Labor Costs Frequently Underestimated

Repair pricing involves more than materials. Labor often represents a significant portion of project costs. Unfortunately, labor-related omissions remain common.

Areas Commonly Underestimated

- Tear-off labor

- Steep roof labor

- High roof charges

- Material handling

- Debris removal

- Cleanup

Each category contributes to the overall project cost. When omitted, the estimate may no longer reflect real-world restoration expenses.

Safety Requirements Add Real Costs

Roofing crews operate in environments that involve genuine risk. Safety requirements often create additional costs that deserve consideration.

Examples include:

- Fall protection systems

- Harness equipment

- Safety monitors

- Specialized access equipment

These expenses are not optional for many projects. They are necessary. And yet they are occasionally absent from initial scopes.

Exterior Damage Beyond the Roof

Hail claims should never focus solely on shingles. The storm impacts the entire property.

Carriers sometimes overlook damage affecting:

- Siding

- Garage doors

- Window screens

- Exterior paint

- Fence systems

- Outdoor structures

A complete inspection examines every affected component. A narrow inspection often leads to supplementation later.

Why Small Omissions Become Big Problems

One missing line item may only represent a few hundred dollars. That does not seem significant. But hail claims rarely involve a single omission. Instead, they involve multiple missing items scattered throughout the estimate.

For example:

| Missing Item | Estimated Cost |

| Starter shingles | $350 |

| Ridge cap | $550 |

| Drip edge | $650 |

| Additional flashing | $900 |

| Vent replacements | $750 |

| Waste factor correction | $1,200 |

Suddenly the estimate may be short by several thousand dollars.And that happens more often than many homeowners realize.

The Real Goal of Supplementing

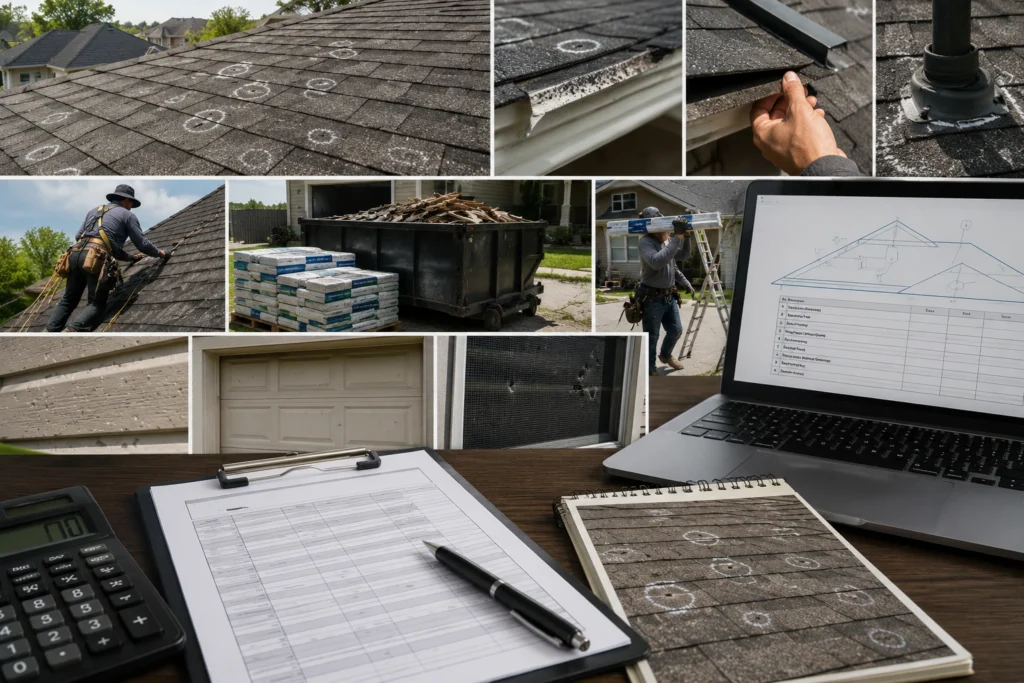

The supplement process is not about conflict. It is not about exaggeration. It is about ensuring the scope reflects the actual work required. Insurance policies generally promise to pay for covered damage. Accurate estimating helps fulfill that promise. When supplements are supported by photographs, measurements, code references, contractor findings, and detailed Xactimate documentation, they provide a path toward a more accurate claim outcome.

Professional Documentation: The Foundation of Every Successful Supplement

A supplement is only as strong as the evidence supporting it. This is where many homeowners run into trouble. They know additional damage exists. Their contractor knows additional damage exists. Yet proving that damage to the insurance carrier requires documentation that is organized, detailed, and persuasive. The strongest supplements are built on facts. Not assumptions.

Comprehensive Photo Documentation

Photographs remain one of the most powerful tools in the claims process. Good photos tell a story. Great photos eliminate doubt.

A complete photo package should include:

- Overview images of all elevations

- Roof slope photographs

- Close-up hail impacts

- Damaged flashing

- Ventilation components

- Soft metal damage

- Gutters and downspouts

- Interior water intrusion if present

The goal is simple. Make it easy for the reviewer to understand exactly what was found and where it was found.

Drone Inspections Improve Visibility

Many roofs contain areas that are difficult to inspect safely.

Drone technology helps capture:

- Steep roof sections

- High elevations

- Large roof systems

- Areas with limited accessibility

High-resolution aerial images often reveal damage patterns that may not be apparent from the ground.

Weather Reports Strengthen the File

Weather verification reports help establish:

- Storm dates

- Hail size

- Wind speeds

- Storm tracks

- Duration of weather events

These reports provide valuable supporting evidence when correlating observed damage with a specific storm event.

Contractor Findings Matter

Experienced roofing contractors frequently uncover conditions that were not visible during the initial carrier inspection.

Examples include:

- Damaged underlayment

- Flashing deficiencies

- Ventilation issues

- Decking concerns

- Installation complications

Detailed contractor reports often become key supplement documents.

The Supplement Submission Process

Many homeowners imagine supplement requests as lengthy disputes. In reality, a properly prepared supplement follows a structured process.

Step 1: Review the Original Estimate

Everything starts with a line-by-line review.

The goal is to identify:

- Missing items

- Quantity discrepancies

- Incorrect measurements

- Pricing concerns

- Code-related omissions

Nothing should be assumed. Every line deserves scrutiny.

Step 2: Create a Detailed Xactimate Estimate

The next step involves preparing a revised estimate that reflects the actual scope of repairs. This estimate should include:

| Category | Purpose |

| Missing line items | Capture overlooked repairs |

| Correct measurements | Improve estimate accuracy |

| Code requirements | Address compliance needs |

| Labor adjustments | Reflect actual installation conditions |

| Material corrections | Ensure proper quantities |

This is where Xactimate expertise becomes particularly valuable. Knowing which line items apply and how they interact can significantly improve estimate accuracy.

Step 3: Assemble Supporting Documentation

Supporting documents typically include:

- Photos

- Inspection reports

- Roof measurements

- Contractor findings

- Weather reports

- Building code references

Strong documentation reduces questions and accelerates review.

Step 4: Submit and Negotiate

After submission, the carrier reviews the supplemental information.Additional inspections may occur. Questions may be asked. Clarifications may be requested. The objective remains straightforward: demonstrate why the additional items are necessary for proper restoration.

Common Homeowner Mistakes During the Supplement Process

Many valid supplements become more difficult because of avoidable mistakes. Let’s look at some of the most common issues.

Assuming the First Estimate Is Final

This happens constantly. A homeowner receives an estimate and assumes the carrier has identified everything. Often, they have not. The first estimate should be viewed as a starting point rather than a final determination. This is especially important when researching What to Do If Your Hail Claim Was Denied, as many denied or underpaid claims may still contain missing damage, measurement errors, overlooked building code requirements, or other issues that can be addressed through additional documentation and supplementation.

Beginning Major Repairs Too Quickly

Emergency mitigation is often necessary. Full restoration is different. Starting extensive repairs before documenting conditions can eliminate important evidence. Once materials are removed, proving the extent of damage becomes more challenging.

Poor Record Keeping

Documentation should be organized from the beginning.

Keep:

- Inspection reports

- Emails

- Photographs

- Estimates

- Invoices

- Weather reports

Good records create a stronger claim file.

Ignoring Code Requirements

Building codes frequently affect restoration costs. Homeowners who overlook code-related issues may unknowingly leave legitimate claim dollars on the table.

Accepting Underpayments Without Review

Many policyholders assume the carrier’s estimate is automatically correct. Sometimes it is. Sometimes it is not. Independent review often reveals opportunities for legitimate supplements.

How Xactimate Expertise Improves Claim Accuracy

There is a reason insurance carriers, contractors, and public adjusters rely on Xactimate. It creates consistency. However, consistency alone does not guarantee accuracy. Knowledge matters. Experience matters. Attention to detail matters.

Understanding Proper Line Items

Xactimate contains thousands of available line items.

Selecting the correct item affects:

- Labor calculations

- Material costs

- Productivity rates

- Project totals

An inaccurate selection can significantly impact claim value.

Identifying Scope Omissions

Experienced estimators learn where omissions commonly occur. They know where to look. They understand roofing systems. They recognize code requirements. Most importantly, they understand how individual components work together.

Presenting Information in a Carrier-Friendly Format

Insurance carriers review claims through structured processes. Supplements presented in familiar Xactimate formats are often easier to evaluate because they align with the carrier’s own estimating framework. This creates clarity. And clarity helps move claims forward.

Why Hail Damage Claim Supplements Matter Financially

The financial impact of a supplement can be substantial. Not because of one major item. Because of many smaller items.

Consider the following example.

| Missed Item | Additional Cost |

| Ridge cap replacement | $600 |

| Starter shingles | $450 |

| Additional flashing | $1,100 |

| Vent replacements | $850 |

| Drip edge installation | $900 |

| Code upgrades | $1,800 |

| Additional labor | $1,400 |

Total supplemental value: $7,100 That is not unusual. In fact, many supplements involve multiple categories of overlooked repairs. Small gaps accumulate quickly.

The Role of Building Codes in Modern Roof Replacements

Building code compliance deserves special attention. A roof replacement is not simply a matter of removing old shingles and installing new ones. Contractors must often comply with current standards.

Common Code-Driven Requirements

Depending on local regulations, projects may require:

- Updated drip edge systems

- Improved ventilation

- Enhanced fastening schedules

- Underlayment upgrades

- Flashing modifications

These requirements create real costs. If the work is necessary, it should be evaluated as part of the restoration scope.

Why Code Issues Surface Later

Code concerns frequently emerge during:

- Permit review

- Contractor planning

- Material ordering

- Construction activities

This is one reason supplements remain common even after estimates have already been approved.

Real-World Indicators That a Supplement May Be Necessary

Not every claim requires supplementation. Many do. Several warning signs often indicate that further review may be beneficial.

Potential Red Flags

- Contractor estimate significantly exceeds carrier estimate

- Missing roof components

- Limited inspection time

- Obvious collateral damage excluded

- Building code concerns

- Measurement discrepancies

- Hidden damage discovered during repairs

If any of these issues appear, additional evaluation may be warranted.

Why Local Knowledge Matters

Storm damage restoration is not identical across every market. Regional conditions influence construction methods, repair costs, and code requirements. Homeowners in League City face weather conditions that can place significant stress on roofing systems over time. Hail events, strong winds, humidity, and coastal exposure all contribute to the complexity of roof claims.

Understanding those local factors often helps identify restoration requirements that generic estimating approaches may overlook. For property owners in League City, a detailed review of hail damage estimates can help ensure all affected components receive proper consideration.

The Difference Between Price and Scope

One of the most misunderstood aspects of insurance claims involves the distinction between pricing and scope. Many people focus on price. The larger issue is often scope.

Price Questions

- Is labor priced correctly?

- Are materials current?

- Are market rates accurate?

Scope Questions

- Is every damaged item included?

- Were measurements completed correctly?

- Are code upgrades addressed?

- Are all repair requirements accounted for?

Scope drives value. If the scope is incomplete, even perfect pricing cannot produce an accurate estimate. This is why Hail Damage Claim Supplements: What Carriers Miss in Their Scope remains such an important conversation. The issue is often not what the carrier included. It is what was left out.

Why Thorough Claim Reviews Benefit Homeowners

Every claim represents a unique property. Every roof system differs. Every storm leaves its own damage pattern. A comprehensive review helps ensure the estimate reflects those realities.

Professional claim reviews often identify:

- Missing components

- Incorrect quantities

- Hidden damage

- Code-related costs

- Labor adjustments

- Documentation gaps

The result is a clearer picture of what restoration truly requires. For homeowners in League City, that level of detail can make a meaningful difference when evaluating hail-related property damage.

Conclusion

Hail claims rarely end with the first estimate. Nor should they. Insurance estimates are prepared using the information available at the time of inspection. As additional evidence emerges, repairs begin, and building requirements become clearer, legitimate supplemental items often surface.

That is why Hail Damage Claim Supplements: What Carriers Miss in Their Scope remains such an important topic for property owners. Missing flashing, ventilation components, underlayment, code upgrades, measurement corrections, labor adjustments, and hidden damage can create substantial gaps between the initial estimate and the true cost of restoration.

The good news is that these gaps can often be identified and documented. Through detailed inspections, organized documentation, and professional Xactimate estimating, supplements provide a pathway toward a more complete and accurate claim outcome. Ultimately, the goal is not to increase a claim unnecessarily. The goal is accuracy. When every damaged component is identified, measured correctly, documented thoroughly, and supported by a detailed estimate, homeowners are in a far better position to restore their property properly and protect the value of their insurance claim.

FAQs

A hail damage claim supplement is a request for additional insurance funds when covered repairs or damage were missed in the original estimate.

High claim volume, limited inspection time, hidden damage, and measurement errors can contribute to incomplete estimates.

Yes. If additional covered damage or required repairs are documented, the carrier may issue additional payment.

Common omissions include flashing, starter shingles, ridge caps, underlayment, ventilation components, and code-required upgrades.

Xactimate provides detailed estimating tools that help identify missing line items, calculate repair costs accurately, and support supplemental requests.

Coverage depends on the policy, but many policies provide coverage for code-required upgrades through ordinance or law provisions.

Compare the scope of work carefully because differences are often caused by missing repair items rather than pricing alone.

The timeline varies depending on the carrier and documentation, but many supplements are reviewed after supporting evidence is submitted.

Yes. Newly discovered covered damage can often be submitted as a supplement if properly documented.

A professional review can help identify scope omissions, code-related costs, measurement errors, and other issues affecting claim accuracy.