Property damage can turn your life upside down in minutes. A storm rolls through League City. A pipe bursts overnight. A kitchen fire spreads faster than expected. Suddenly you’re dealing with repairs, paperwork, inspections, and insurance calls.

This is exactly when homeowners start asking an important question: when to hire a public adjuster.

Insurance claims may look simple on paper, but the reality is very different. Policies are complex. Damage assessments are technical. And negotiations with insurers can become stressful quickly.

I’ve seen many homeowners assume their insurance company will handle everything smoothly. Sometimes they do. Other times the claim becomes complicated, delayed, or undervalued.

That’s where a public adjuster steps in.

Understanding when to hire a public adjuster can make a major difference in the outcome of your insurance claim. In many cases, the right timing can mean the difference between a minimal payout and a settlement that truly covers your losses.

Let’s break it down.

Understanding the Role of a Public Adjuster

Before deciding when to hire a public adjuster, it’s important to understand what they actually do.

A public adjuster is a licensed professional who works on behalf of policyholders—not insurance companies. Their job is to evaluate property damage, prepare insurance claims, and negotiate settlements with insurers.

Insurance companies employ adjusters too. But those adjusters represent the insurance company’s interests.

Public adjusters represent yours.

What a Public Adjuster Handles

A qualified public adjuster typically manages several important tasks during a claim:

- Inspecting property damage in detail

- Reviewing your insurance policy coverage

- Estimating repair costs

- Documenting losses with photos and reports

- Preparing claim documentation

- Negotiating settlements with insurers

In short, they level the playing field.

Public Adjuster vs Insurance Company Adjuster

Many homeowners assume the adjuster assigned by their insurance company is working for them. That’s not exactly how it works.

Here’s the difference.

| Type of Adjuster | Who They Work For | Main Goal |

| Insurance Company Adjuster | Insurance company | Protect insurer’s financial interests |

| Independent Adjuster | Insurance company (contracted) | Evaluate claims for insurer |

| Public Adjuster | Homeowner or policyholder | Maximize policyholder claim settlement |

This distinction is crucial when deciding when to hire a public adjuster. The earlier you understand this dynamic, the better you can protect your claim.

When to Hire a Public Adjuster

Timing matters. Hiring a public adjuster too late can limit what they can do. Hiring one at the right moment can dramatically improve your claim outcome.

Here are the most common scenarios.

After Major Property Damage

Large losses often involve complicated claims.

Storm damage. Fire damage. Flooding. Structural issues.

These claims require detailed documentation, repair estimates, and negotiations.

A public adjuster can perform a full property inspection and identify damage that might otherwise be missed.

Common major damage scenarios include:

- Hurricane damage

- Wind and roof damage

- Flood-related structural damage

- Fire or smoke damage

- Large water damage losses

If your home has suffered significant damage, it’s usually a strong sign of when to hire a public adjuster.

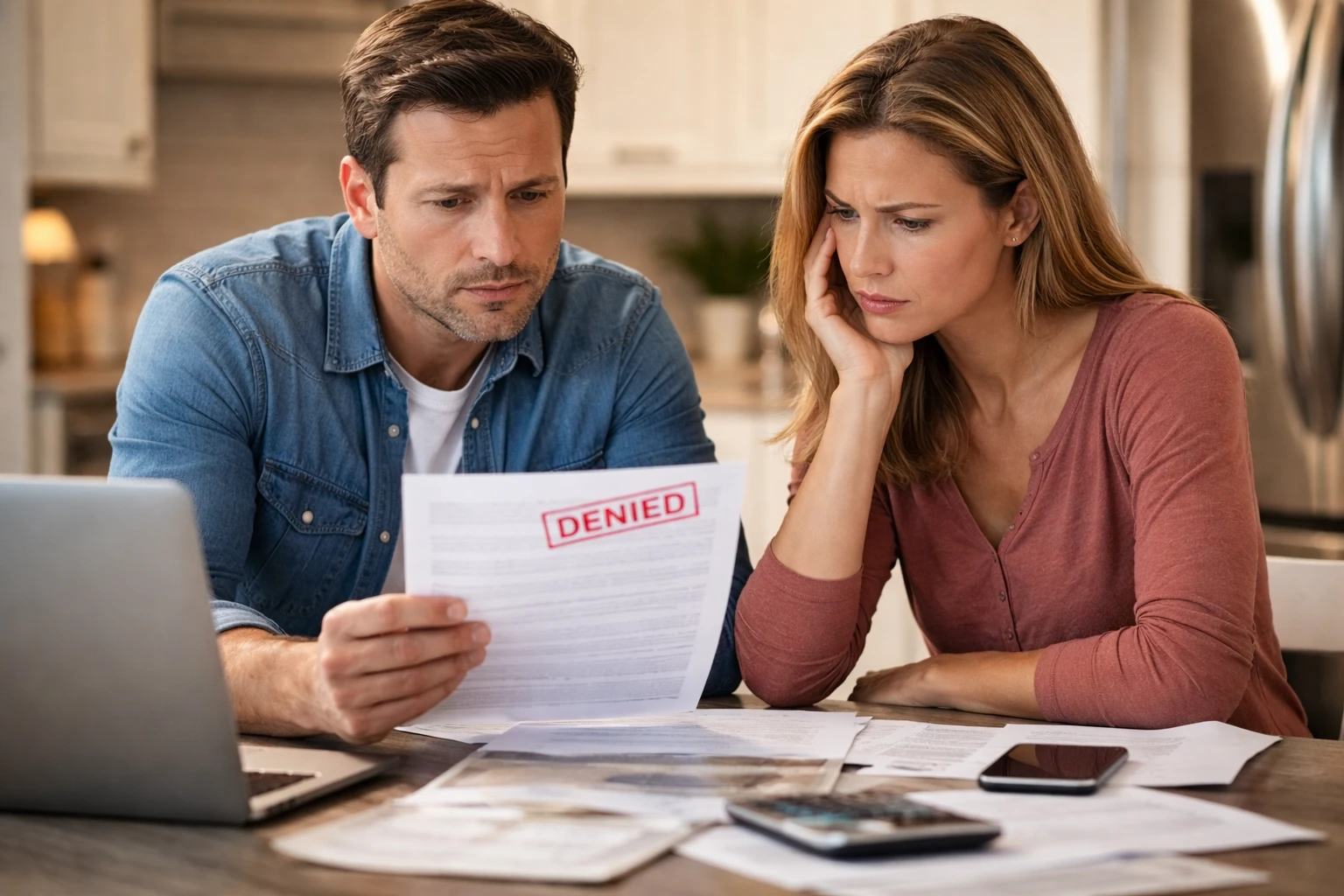

When Your Insurance Claim Is Denied

Claim denials happen more often than homeowners expect.

Sometimes it’s due to missing documentation. Other times it’s because the insurer interprets the policy differently than the homeowner.

A public adjuster can review the denial and determine whether the claim should have been covered.

They may uncover issues such as:

- Incorrect policy interpretation

- Missed damage categories

- Incomplete inspection reports

- Documentation errors

In these situations, understanding when to hire a public adjuster becomes critical. The sooner you bring in professional help, the better your chances of resolving the claim.

When the Insurance Settlement Seems Too Low

One of the most common reasons homeowners seek help is a low settlement offer.

Insurance companies often make an initial offer based on their own inspection. That estimate may not include every repair or hidden damage.

A public adjuster can re-evaluate the property and prepare a more accurate damage assessment.

For example:

| Damage Type | Insurance Estimate | Public Adjuster Estimate |

| Roof replacement | $8,000 | $18,000 |

| Interior repairs | $4,500 | $12,000 |

| Structural repairs | $3,000 | $10,000 |

These differences happen because damage is sometimes underestimated.

Knowing when to hire a public adjuster in these cases can help ensure the settlement reflects the true cost of restoring your property.

When the Claims Process Becomes Overwhelming

Insurance claims involve a surprising amount of work.

Phone calls. Documentation. Contractor estimates. Follow-up inspections.

For homeowners already dealing with damage and repairs, the process can become overwhelming.

Here are some common frustrations:

- Endless paperwork

- Delayed insurance responses

- Confusing policy language

- Multiple inspections

A public adjuster takes over much of this responsibility.

They communicate with the insurance company. They organize documentation. And they negotiate the claim.

This is another major indicator of when to hire a public adjuster—when managing the claim becomes too difficult to handle alone.

When You Lack Experience With Insurance Claims

Most homeowners rarely file large insurance claims.

The process can be unfamiliar and confusing.

Insurance policies contain technical language that isn’t always easy to interpret.

Public adjusters understand policy wording and coverage categories. They know what insurers look for in documentation.

That experience matters.

If you’ve never handled a large property claim before, it may be exactly when to hire a public adjuster.

Situations Common in League City Where Public Adjusters Help

League City sits along the Texas Gulf Coast, which means homeowners face unique property risks.

Storms alone can create major insurance claims.

Hurricane and Tropical Storm Damage

Strong winds and heavy rain can damage:

- Roofing systems

- Exterior siding

- Windows and doors

- Interior ceilings and drywall

Hurricanes often cause layered damage that takes time to fully identify.

Public adjusters frequently help homeowners document these losses properly.

Flood and Water Damage

Flooding can come from multiple sources:

- Storm surge

- Heavy rainfall

- Plumbing failures

- Roof leaks

Water damage also creates hidden problems like mold or structural weakening.

A thorough inspection is critical when deciding when to hire a public adjuster.

Fire and Smoke Damage

Fire claims are complex.

Even when flames damage only part of a home, smoke contamination can spread throughout the property.

Claims may include:

- Structural repairs

- Smoke cleanup

- Personal property replacement

- Temporary housing costs

Public adjusters often play a key role in documenting these losses.

Roof and Hail Damage

Roof damage is one of the most disputed types of insurance claims.

Insurers may argue that damage is due to age rather than storms.

A public adjuster can gather inspection reports, contractor estimates, and weather documentation to support your claim.

Signs You Should Call a Public Adjuster Immediately

Some situations demand immediate professional assistance.

Watch for these warning signs.

- The insurance company delays your claim response

- The damage estimate seems incomplete

- Multiple types of damage are involved

- Your insurer requests extensive documentation

- Settlement negotiations stall

If any of these occur, it may be exactly when to hire a public adjuster.

When You Might Not Need a Public Adjuster

Public adjusters provide tremendous value, but not every claim requires one.

Small and straightforward claims may not need professional assistance.

Examples include:

- Minor roof repairs

- Small plumbing leaks

- Cosmetic damage

- Simple appliance failures

If the claim is low value and easily resolved, homeowners may handle it themselves.

Still, understanding when to hire a public adjuster ensures you know when expert help becomes worthwhile.

How a Public Adjuster Helps Maximize Your Claim

A skilled public adjuster adds value in several ways.

Detailed Damage Assessment

They inspect every area of the property.

Not just visible damage.

Hidden issues often include:

- Water intrusion

- Structural movement

- Electrical damage

- Insulation contamination

Documentation and Evidence Collection

Insurance claims rely on documentation.

Public adjusters compile:

- Photographs

- Repair estimates

- Damage reports

- Contractor evaluations

Strong documentation supports stronger claims.

Policy Interpretation

Insurance policies contain multiple coverage categories.

These may include:

- dwelling coverage

- personal property coverage

- loss of use coverage

- additional living expenses

A public adjuster ensures the claim includes every eligible category.

Negotiating With Insurance Companies

Negotiation is where public adjusters often make the biggest impact.

They present evidence, repair estimates, and policy interpretations to support the claim.

Insurance companies take these negotiations seriously because public adjusters understand the process.

What Happens After You Hire a Public Adjuster

Hiring a public adjuster follows a structured process.

Here’s how it typically works.

Step 1: Initial Consultation

The adjuster reviews your insurance policy and discusses the damage.

Step 2: Property Inspection

A detailed inspection identifies all damage.

Step 3: Claim Preparation

Documentation, estimates, and reports are compiled.

Step 4: Claim Submission

The adjuster submits the claim to the insurance company.

Step 5: Negotiation

The adjuster negotiates settlement terms with the insurer.

Step 6: Claim Resolution

Once an agreement is reached, the insurance payout is finalized.

This process highlights exactly when to hire a public adjuster—before negotiations become difficult.

How to Choose the Right Public Adjuster in League City

Choosing the right professional matters.

Look for these key qualifications.

Verify Licensing

Public adjusters in Texas must be licensed by the state.

Evaluate Experience

Experience with Gulf Coast claims is extremely valuable.

Understand Their Fee Structure

Most public adjusters charge a contingency fee, meaning they are paid a percentage of the claim settlement.

Check Reputation

Look for:

- customer reviews

- testimonials

- professional references

Common Misconceptions About Public Adjusters

Many myths surround public adjusters.

Let’s clear up a few.

Myth: They Are Only for Commercial Claims

Residential homeowners frequently use public adjusters for large losses.

Myth: Hiring One Slows the Claim

In many cases, professional documentation speeds up the process.

Myth: Insurance Companies Dislike Them

Policyholders have the legal right to representation.

Understanding these misconceptions helps clarify when to hire a public adjuster.

Cost of Hiring a Public Adjuster

Public adjusters typically work on contingency.

That means they receive a percentage of the settlement.

Typical fee ranges:

| Claim Size | Typical Fee |

| Small claim | 10–20% |

| Medium claim | 8–15% |

| Large claim | 5–10% |

Many homeowners find the higher settlement offsets the fee.

Practical Tips for Homeowners Filing Insurance Claims

If you’re preparing to file a claim, follow these best practices.

- Document damage immediately with photos and videos

- Keep receipts for emergency repairs

- Avoid permanent repairs until inspections are complete

- Maintain records of insurer communication

- Read your policy carefully

These steps help protect your claim while you evaluate when to hire a public adjuster.

Final Thoughts: Protecting Your Insurance Claim

Property damage is stressful. Insurance claims can make it even more complicated.

But the process becomes much easier when you understand when to hire a public adjuster.

Large claims. Denied claims. Low settlement offers. Complex damage.

These are all situations where professional representation can make a major difference.

Homeowners in League City face unique risks from storms, water damage, and coastal weather. When serious damage occurs, having an experienced advocate can help ensure your insurance claim truly reflects the cost of rebuilding your home.

And sometimes, that’s exactly what makes the difference between a frustrating claim and a fair recovery.

FAQs

A public adjuster represents the policyholder during an insurance claim, helping assess damage, prepare documentation, and negotiate with the insurance company for a fair settlement.

You should consider hiring one after major property damage, if your claim is denied, or if the insurance settlement seems too low.

Yes, homeowners can hire a public adjuster at any stage of the claim process, although earlier involvement often leads to better claim preparation.

No, public adjusters work exclusively for policyholders and advocate for the homeowner’s interests during the claims process.

Most public adjusters charge a contingency fee, typically ranging from 5% to 20% of the final insurance settlement.

For minor damage or straightforward claims, homeowners may be able to handle the process themselves without professional assistance.

In many cases, a public adjuster can actually speed up the process by ensuring documentation is complete and negotiations are handled efficiently.

Yes, public adjusters can review the denial, reassess the damage, and help reopen or dispute the claim if coverage should apply.

Yes, public adjusters must be licensed by the state of Texas and comply with state regulations governing insurance claim representation.

If your property damage is significant, the claims process becomes complicated, or you feel the settlement is unfair, it may be the right time to hire a public adjuster.