Hailstorms can turn a normal day in League City into a stressful insurance situation in minutes. One storm rolls through, your roof takes a beating, and suddenly you’re trying to understand estimates, inspections, policy language, and claim paperwork. That’s exactly why understanding Public Adjuster vs. Insurance Adjuster for Hail Claims in League City, TX is so important. Many homeowners assume every adjuster involved in a claim works for them. They don’t.

In fact, one of the most misunderstood parts of the hail claim process is knowing who represents whose interests. That distinction can influence inspections, claim valuations, repair recommendations, and ultimately the amount paid on a covered loss. If you’ve recently experienced hail damage in League City, this guide will help you understand the differences between public adjusters and insurance adjusters, when each professional becomes involved, and how to determine which option may be best for your specific situation.

Understanding Hail Damage Claims in League City

League City residents are no strangers to severe weather. The Gulf Coast regularly experiences storms capable of producing hail, high winds, torrential rain, and flying debris. While some hailstones leave obvious dents and broken shingles, others create subtle damage that may not be immediately visible from the ground.

That’s where problems often begin. A roof can appear perfectly fine while sustaining hidden bruising, granule loss, compromised flashing, and weakened roofing materials that shorten its lifespan. When damage isn’t obvious, the claims process becomes more dependent on inspections, documentation, and professional opinions.

Why Hail Damage Can Be Difficult to Evaluate

Unlike a broken window, hail damage isn’t always straightforward.

Several factors affect the severity of roof damage:

- Hail size

- Wind speed

- Roof age

- Roofing material type

- Impact angle

- Storm duration

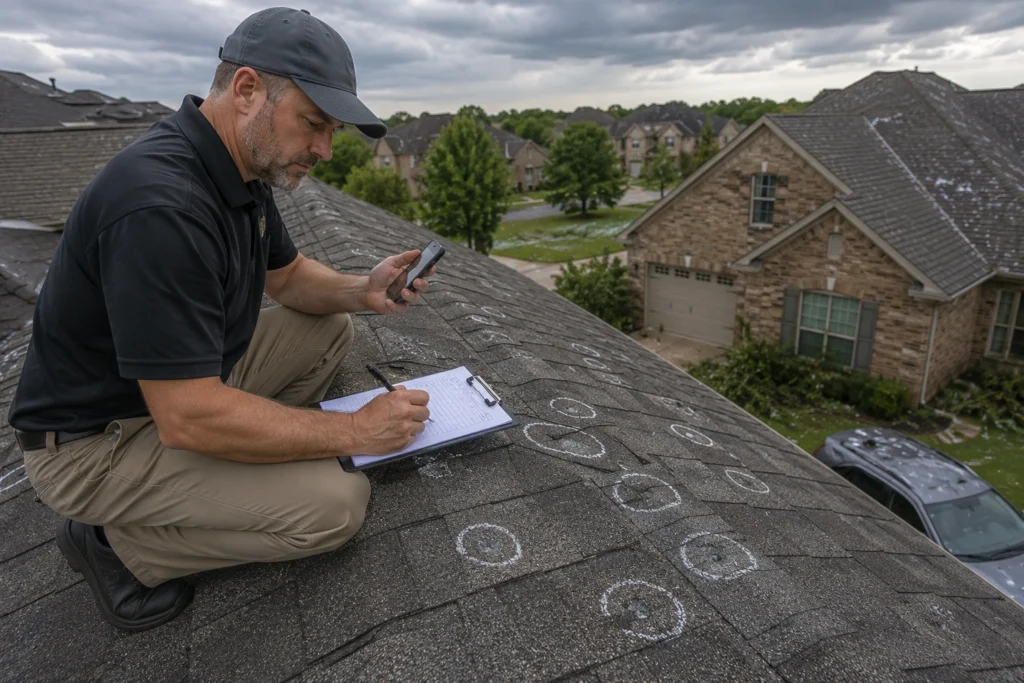

Two neighboring homes can experience very different levels of damage despite being exposed to the same storm. Because of this, inspections matter. A lot. Evaluating storm damage sometimes resembles a process of forensic analysis, where inspectors must examine subtle evidence, identify impact patterns, and distinguish storm-related damage from normal aging and wear.

The Typical Hail Claim Process

Most homeowners follow a similar path after a storm.

| Step | Description |

| Damage Occurs | Hail impacts roof and property |

| Claim Filed | Homeowner contacts insurer |

| Inspection Scheduled | Adjuster visits property |

| Estimate Prepared | Scope of damage developed |

| Settlement Offered | Carrier issues payment determination |

| Repairs Completed | Contractor performs work |

| Supplemental Review | Additional damage may be discovered |

While the process looks simple on paper, disagreements can arise at nearly every stage.

Why Some Hail Claims Become Disputed

Not every hail claim ends with immediate agreement. In fact, many homeowners become frustrated when they discover the insurer’s estimate differs significantly from contractor findings.

Common sources of disagreement include:

- Roof replacement versus repair

- Missed damage

- Underestimated repair costs

- Code upgrade requirements

- Matching issues

- Cosmetic damage arguments

- Supplemental repairs

The larger the claim becomes, the more likely multiple opinions enter the conversation. That is where understanding the difference between adjusters becomes essential.

What Is an Insurance Adjuster?

An insurance adjuster is a professional assigned to investigate and evaluate an insurance claim on behalf of an insurance company. Their role is important. Without adjusters, claims could not be processed efficiently. However, homeowners often misunderstand who these professionals represent. The insurance adjuster works for the insurance carrier. Their responsibility is to evaluate the claim according to policy provisions, company procedures, and available evidence.

Types of Insurance Adjusters

Not all insurance adjusters work the same way.

Staff Adjusters

Staff adjusters are direct employees of the insurance company. They receive salaries and benefits from the carrier. Their job involves evaluating claims and recommending settlements based on company guidelines.

Independent Adjusters

Independent adjusters are not employees but work under contract for insurance carriers. These adjusters are frequently deployed after major storms when claim volume increases dramatically. Following large hail events in League City, independent adjusters often assist carriers with handling hundreds or even thousands of inspections.

What Insurance Adjusters Actually Do

Many homeowners imagine adjusters simply climbing onto roofs. The reality is much broader.

Insurance adjusters typically:

- Inspect property damage

- Photograph affected areas

- Review policy coverage

- Prepare estimates

- Document findings

- Communicate claim decisions

- Recommend payment amounts

They serve a critical function within the insurance system. But their role has limits.

Strengths of Insurance Adjusters

Insurance adjusters provide several benefits.

These include:

- Fast claim response

- Organized claim handling

- Standardized estimating methods

- Policy interpretation expertise

- Coordination with claim departments

Many claims move smoothly because adjusters efficiently gather information and process settlements. When damage is obvious and uncontested, the process can work very well.

Potential Limitations Homeowners Should Understand

Even skilled adjusters face challenges. After severe storms, adjusters may handle dozens of inspections each week. Time becomes limited. Large claim volumes create pressure. No inspection process is perfect. As a result, some damage may be overlooked, underestimated, or disputed. This does not necessarily mean anyone acted improperly. It simply reflects the reality of evaluating complex property losses under demanding conditions.

What Is a Public Adjuster?

A public adjuster is a licensed insurance claim professional who represents policyholders rather than insurance companies. That distinction changes everything. Instead of working for the carrier, the public adjuster works exclusively for the homeowner or business owner. Their goal is to help the insured document, prepare, and negotiate a covered claim.

How Public Adjusters Differ

The easiest way to understand the difference is this: Insurance adjusters represent the insurer. Public adjusters represent the policyholder. That’s it. That single distinction influences every aspect of the claims process.

Responsibilities of a Public Adjuster

Public adjusters often become involved when claims become complex, disputed, delayed, or underpaid.

Their responsibilities may include:

- Reviewing insurance policies

- Inspecting property damage

- Preparing claim documentation

- Developing detailed estimates

- Managing communications

- Negotiating settlements

- Identifying supplemental damages

Rather than focusing solely on the initial inspection, public adjusters often remain involved throughout the entire claim process.

How Public Adjusters Are Paid

Most public adjusters work on a contingency basis. This means compensation is typically based on a percentage of the claim recovery. If no recovery occurs, fees may not be owed depending on contract terms. Homeowners should always review fee agreements carefully before signing. Understanding costs upfront prevents misunderstandings later.

Why Homeowners Hire Public Adjusters

Several situations commonly lead homeowners to seek representation.

For example:

- Significant roof damage

- Large losses

- Claim denials

- Underpaid settlements

- Complex policy questions

- Multiple damaged structures

- Commercial property claims

In many cases, homeowners simply want professional guidance through an unfamiliar process. And that’s understandable. Most people file very few property claims during their lifetime.

Public Adjuster vs. Insurance Adjuster for Hail Claims in League City, TX

Now let’s compare the two side by side. Understanding these differences can help homeowners make informed decisions after a storm.

| Category | Public Adjuster | Insurance Adjuster |

| Represents | Policyholder | Insurance Company |

| Hired By | Homeowner | Insurance Carrier |

| Primary Objective | Advocate for insured | Evaluate claim for insurer |

| Reviews Policy Benefits | Yes | Yes |

| Negotiates Settlement | Yes | No |

| Manages Entire Claim | Often | Typically No |

| Paid By | Policyholder agreement | Insurance Company |

| Works Exclusively for Homeowner | Yes | No |

This table highlights why the phrase Public Adjuster vs. Insurance Adjuster for Hail Claims in League City, TX matters so much. Although both professionals evaluate damage, they serve different interests and perform different functions throughout the claim process.

Who Works for Whom?

Many homeowners skip this question. They shouldn’t. It may be the most important concept in the entire article.

Insurance Adjusters Serve the Carrier

Insurance companies hire adjusters to investigate claims and determine covered damages under the policy. Their responsibility is to the insurance company that employs or contracts with them. That does not mean they are adversaries. Far from it. Most adjusters strive to evaluate claims fairly. However, they are not personal advocates for the homeowner.

Public Adjusters Serve the Policyholder

Public adjusters work directly for the insured. Their responsibility is to help the policyholder understand coverage, document damage, and pursue the claim. Because their role centers on representation, they often spend additional time reviewing damage scopes, contractor findings, and repair requirements. This difference frequently becomes significant when disagreements emerge regarding roof replacement, code compliance, or supplemental damage.

How Each Adjuster Evaluates Hail Damage

At first glance, two adjusters inspecting the same roof may appear to be doing identical work. They’re not. The process, priorities, and objectives can differ considerably. That difference often affects how damage is documented and how repair recommendations are developed.

How Insurance Adjusters Typically Inspect Hail Damage

Insurance adjusters generally follow established company procedures.

Their inspections often include:

- Roof measurements

- Shingle evaluation

- Collateral damage review

- Photographs

- Damage mapping

- Estimate preparation

Most carriers use estimating software to create repair scopes and determine pricing. The inspection is designed to identify covered damage and establish what the insurer believes is necessary to restore the property under policy terms. For straightforward claims, this process may work very well. However, hail damage is not always straightforward.

How Public Adjusters Typically Inspect Hail Damage

Public adjusters often approach inspections differently. Because they represent the policyholder, their focus is generally on identifying all covered damage that may affect the claim.

A detailed inspection may include:

- Roofing materials

- Flashing systems

- Ridge caps

- Gutters

- Downspouts

- Window screens

- HVAC equipment

- Exterior finishes

- Interior water intrusion

The goal is not simply to identify obvious impacts. The goal is to understand the full scope of storm-related damage. That distinction matters.

Areas Commonly Overlooked After Hailstorms

Not every roof issue is visible from the ground.

Some of the most frequently disputed items include:

| Area | Potential Issue |

| Ridge caps | Impact fractures |

| Flashing | Functional damage |

| Gutters | Dents and displacement |

| Roof vents | Metal impact damage |

| Soft metals | Evidence of hail activity |

| Skylights | Cracks and seal damage |

| HVAC units | Coil damage |

| Underlayment | Hidden moisture concerns |

When these items are missed initially, supplemental claims may become necessary later.

When Homeowners Often Rely on the Insurance Adjuster Alone

Not every claim requires additional representation. Sometimes the process proceeds smoothly from beginning to end.

Minor Hail Damage Claims

If a roof sustains limited damage requiring only small repairs, the insurance company’s adjuster may provide an adequate scope and settlement.

Examples include:

- Isolated shingle damage

- Minor gutter repairs

- Small accessory replacements

Simple claims often resolve quickly. And that’s a good thing.

Clear and Undisputed Damage

Some losses are obvious. When significant damage is clearly visible and both parties agree on repairs, disputes are less likely to arise. In these situations, homeowners may feel comfortable proceeding without additional representation.

Advantages of Keeping the Process Simple

There are benefits to avoiding unnecessary complexity.

These include:

- Fewer parties involved

- Faster claim resolution

- Lower administrative burden

- No public adjuster fees

For many homeowners, that simplicity is appealing. The key is ensuring the settlement accurately reflects the damage.

When Hiring a Public Adjuster May Make Sense

Not every hail claim is simple. Far from it. As claim complexity increases, many homeowners begin exploring professional representation.

Large Roof Replacement Claims

A full roof replacement can involve substantial costs. When replacement recommendations differ between contractors and insurers, disputes often emerge.

Questions may include:

- Is repair sufficient?

- Is replacement necessary?

- Are matching issues present?

- Have all damaged slopes been identified?

These discussions can significantly affect claim value.

Underpaid Insurance Settlements

One of the most common reasons homeowners contact public adjusters is concern over an underpaid claim.

Signs may include:

- Contractor estimates far exceed insurer estimates

- Missing line items

- Incomplete repair scopes

- Excluded damage categories

A second review can help determine whether additional documentation may be needed.

Denied Hail Claims

Claim denials create immediate frustration. Especially when visible damage appears obvious.

Common denial reasons include:

- Insufficient evidence

- Wear and tear findings

- Late reporting

- Coverage exclusions

- Causation disputes

In these situations, policyholders often seek professional guidance regarding next steps.

Commercial Property Claims

Commercial hail losses are often more complicated than residential claims.

Potential issues include:

- Multiple roof systems

- Tenant concerns

- Business interruption impacts

- Mechanical equipment damage

- Extensive documentation requirements

As claim complexity grows, specialized expertise often becomes more valuable.

Supplemental Damage Discovery

Some storm damage is discovered only after repairs begin.

For example:

A contractor removes roofing materials and discovers:

- Damaged decking

- Wet insulation

- Hidden flashing failures

- Structural concerns

Additional claim submissions may be required.

This is commonly referred to as supplementing the claim. In many cases, Hail Damage Claim Supplements become necessary after contractors begin repairs and uncover hidden storm-related issues that were not visible during the initial inspection. These supplemental requests can include damaged decking, wet insulation, flashing problems, or other covered repairs that were not included in the original estimate.

Common Hail Claim Scenarios in League City

Every property is different. However, certain claim disputes appear repeatedly throughout League City and the surrounding Gulf Coast region.

Scenario One: Roof Repair Versus Roof Replacement

This may be the most common disagreement. The insurance company concludes repairs are adequate. The contractor recommends replacement.

Now what?

The answer depends on:

- Extent of damage

- Material condition

- Repair feasibility

- Manufacturer guidance

- Building code requirements

Proper documentation becomes critical.

Scenario Two: Cosmetic Damage Arguments

Metal surfaces often generate debate.

For example:

- Gutters

- Roof vents

- Flashing

- Metal roofing systems

Insurers may argue dents are cosmetic. Property owners may argue the damage affects appearance, value, and long-term performance. Coverage depends heavily on policy language and damage characteristics.

Scenario Three: Matching Problems

Older roofing products create unique challenges. Sometimes replacement shingles simply no longer exist. Even when repair is technically possible, matching may be impossible.

This can create disputes involving:

- Color consistency

- Texture consistency

- Material availability

The issue becomes especially important on highly visible roof slopes.

Scenario Four: Wind and Hail Combined Damage

League City storms rarely involve hail alone.

Strong winds frequently accompany severe weather events.

As a result, roofs may suffer multiple forms of damage simultaneously.

Potential issues include:

- Creased shingles

- Lifted tabs

- Missing shingles

- Impact damage

- Water intrusion

Properly distinguishing storm damage from age-related deterioration becomes essential.

The Financial Question: Is Hiring a Public Adjuster Worth It?

This is often the first question homeowners ask. And understandably so. The answer depends on the specific claim.

Understanding Public Adjuster Fees

Most public adjusters charge a percentage-based fee. Fee structures vary.

Homeowners should carefully review:

- Percentage rates

- Contract terms

- Cancellation provisions

- Service scope

Transparency matters. Any professional should clearly explain fees before representation begins.

Situations Where Representation May Provide Value

Public adjusters may provide value when:

- Claims are large

- Coverage issues exist

- Settlement disputes arise

- Documentation requirements become extensive

- Multiple inspections are needed

In these situations, professional claim management may help reduce stress while improving organization.

Situations Where Representation May Be Less Necessary

Some claims simply do not require extensive assistance.

Examples may include:

- Minor repairs

- Straightforward settlements

- Quickly approved claims

- Limited damage losses

The goal should always be making an informed decision based on claim complexity. Not fear. Not pressure. Just facts.

Texas Regulations and Consumer Protections

Texas regulates public adjusters through licensing requirements and consumer protection rules. That oversight exists for a reason. Homeowners deserve protection.

Licensing Matters

Always verify licensing before hiring any public adjuster.

A properly licensed professional should willingly provide:

- License information

- Contact details

- Experience background

- Contract documentation

Verification helps ensure accountability.

Questions Every Homeowner Should Ask

Before hiring representation, ask:

- How many hail claims have you handled?

- How long have you worked in Texas?

- What is your fee structure?

- How will communication occur?

- What services are included?

Clear answers help establish expectations from the start.

Red Flags to Watch For

Be cautious when you encounter:

- High-pressure sales tactics

- Unrealistic promises

- Guaranteed outcomes

- Requests to sign immediately

- Lack of licensing information

Professional representation should be built on trust and transparency. Not urgency.

How to Choose the Right Public Adjuster in League City

If you decide additional representation may be beneficial, selection matters. A lot. Not all adjusters have the same experience, communication style, or hail claim expertise.

Verify Local Experience

League City presents unique challenges. An adjuster familiar with Gulf Coast weather patterns, local contractors, and regional roofing systems may bring valuable insight.

Ask specifically about:

- Hail claims

- Wind claims

- Roof replacement disputes

- Local property types

Experience is difficult to replace.

Review Their Process

A quality public adjuster should clearly explain:

- Inspection procedures

- Documentation methods

- Communication expectations

- Negotiation approach

If explanations are vague, continue asking questions. You deserve clarity.

Evaluate Communication

Claims can last weeks or months. Choose someone who communicates effectively.

Look for:

- Prompt responses

- Clear explanations

- Regular updates

- Professional conduct

Technical knowledge is important. Communication is equally important.

Steps Homeowners Should Take Before Making Any Decision

Whether you ultimately hire a public adjuster or proceed independently, several actions can strengthen your position.

Schedule a Thorough Roof Inspection

Professional inspections can identify damage that may not be visible from the ground. The sooner damage is documented, the better.

Photograph Everything

Create a visual record.

Include:

- Roof damage

- Gutters

- Downspouts

- Fencing

- HVAC equipment

- Interior leaks

Good documentation often becomes valuable later.

Review Your Insurance Estimate Carefully

Do not simply focus on the payment amount. Read the scope. Line by line.

Understand:

- What was included

- What was excluded

- What was depreciated

- What may require supplements

Ask Questions

Never hesitate to seek clarification. A quality claims process should be transparent. If something seems unclear, ask. Then ask again. Understanding your claim is one of the best ways to protect your interests.

FAQs

A public adjuster represents the policyholder, while an insurance adjuster represents the insurance company during the claims process.

No. Minor and straightforward claims often resolve successfully without additional representation.

Yes. Many homeowners hire a public adjuster after receiving an estimate, settlement offer, or claim denial.

Most public adjusters work on a contingency fee basis and are paid a percentage of the claim recovery.

Yes. A public adjuster can review the scope of damage and determine whether additional covered items may have been missed.

You can request clarification, provide additional documentation, or seek professional assistance to evaluate your options.

Yes. Contractors sometimes uncover concealed damage during repairs that was not visible during the initial inspection.

They are additional claim submissions for covered damage discovered after the original estimate was prepared.

Yes. Public adjusters must meet state licensing requirements and comply with Texas regulations.

It can be beneficial when claims involve significant damage, disputes, complex coverage issues, or settlement disagreements.